Blockchain – a topic that is kind of overshadowed by its famous application in the past couple of years, and could fundamentally change the world as we know it. But ask someone on the street to try explaining the concept, and more likely than not it would be met with blank stares and stuttered response. So, I will try to communicate some understanding about the concept in 5 main points.

My readings will be from WIRED, Harvard Business Review, Bloomberg, and two other individual authors – Hayley Somerville (https://www.linkedin.com/in/hayleysomerville/) and Tony Yin (https://www.linkedin.com/in/tonyin/). The references will be included below.

What is the subject about?

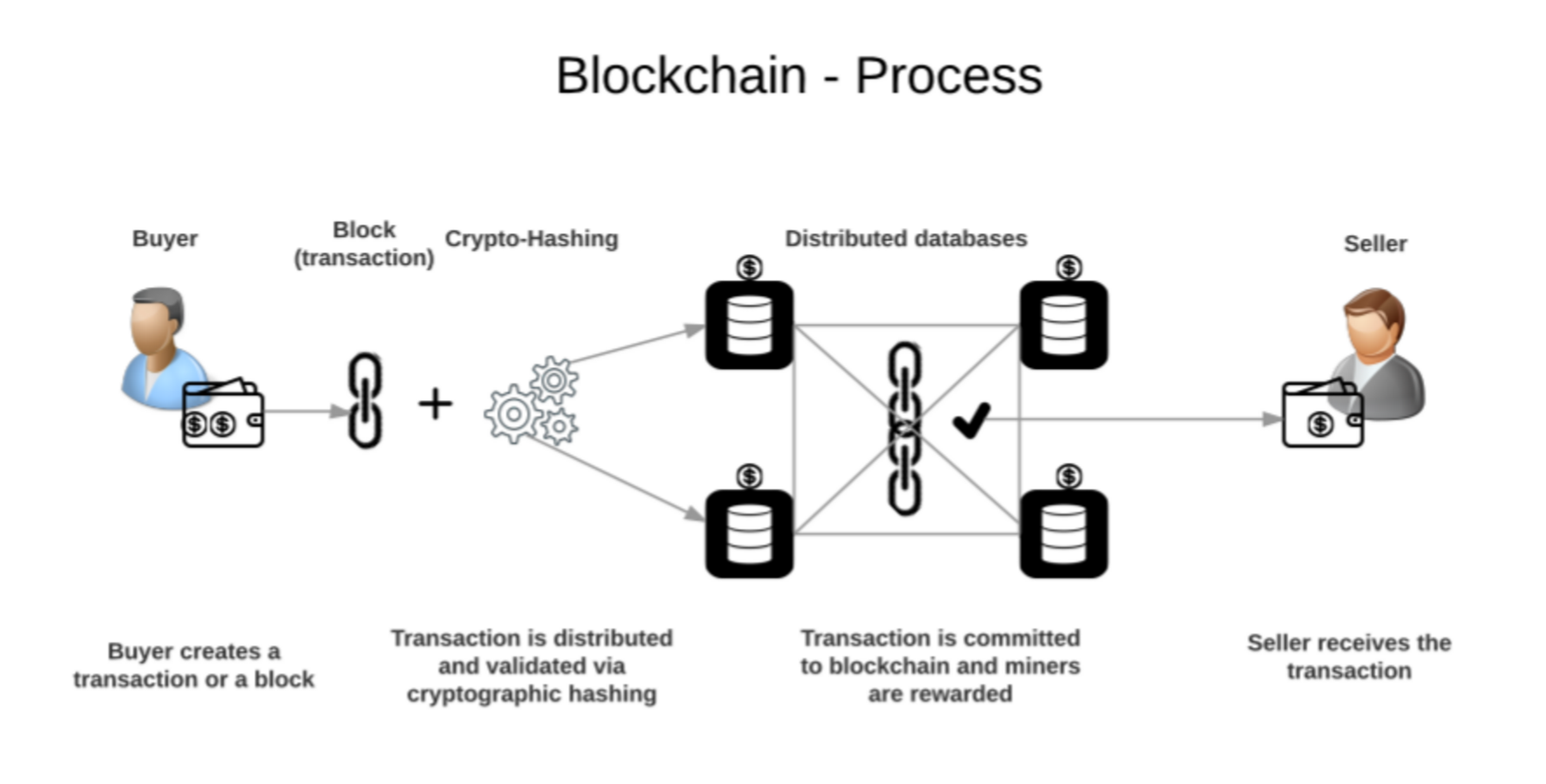

When it comes to explaining blockchain, the technical definition would obviously involve the words “block” and “chain”. But on a more general and conceptual level, it is explained as an “open, distributed/decentralised, digital ledger of transactions”. And for those who may not be that familiar, ledger is like a notebook to record transactions, and previously was more common in the world of accounting (and still is).

So how does a notebook containing transactions be open and distributed? While the more intricate details will be explained in the next point, for now we will understand it as such: the ledger is replicated, and an identical copy is stored on each computer that makes up the blockchain network – and when there are changes to one copy, all other copies will be updated simultaneously.

How does it work?

Harvard Business Review has nicely outlined 5 basic principles in explaining how blockchain works:

- Distributed Database: In a blockchain network (made up of multiple parties on the computers), each party has access to the whole database and its complete history. Distributed also means no single party controls the data or the information, but every party verifies the records in the database without any middleman.

- P2P Transmission: Instead of going through a central node (point), communication is done between peers (the earlier mentioned parties/computers) where each node stores and forwards information to all other nodes.

- Transparency with Pseudonymity: Transparency – every transaction is visible to anyone with access to the system; pseudonymity – each node on a blockchain has a unique alphanumeric address that identifies it (instead of names), and transactions occur between these addresses.

- Irreversibility of Records: Records of completed transactions are linked (hence, the “chain”) to every transaction record that came before them. This way, the transactions are locked, and to alter would require altering the records that came before them (before new transactions attaches to them). To add on further, various computational algorithms ensure the recording is permanent (or super-duper difficult to crack), chronologically ordered, and available to all others in the network.

- Computational Logic: Users can set up alogrithms and rules that automatically trigger transactions between nodes. (This feature will be explained further in the following points about application).

Now, many may still find it difficult to visualise how this works from the 5 principles, which explains why there are articles such as “Explained Like I’m 5: Blockchain”, and a video of an expert explaining blockchain in 5 different difficulty levels.

In one “Explained Like I’m 5” article, Hayley Somerville used an example of schoolchildren trying to track lunch IOUs (an informal note on who-owes-what) between each other. The problem was this particular child was owing lunches all-around after asking for bits and pieces of lunch from the other children, but did not reciprocate by offering parts of his lunch to others. Without an IOU recorded somewhere, he could get away with it. But relying on a central IOU notebook (held by a teacher who conveniently sleeps during recess), the child exploits the fallibility of the sleeping teacher to alter the records in this notebook.

The solution then is to invent an electronic IOU notebook via a mobile app used by the whole class of children, where every time a person adds an IOU, it goes to everyone’s phone at the same time (and no one can change the truth, because everyone knows the truth – the same list of all the IOUs, and which phone number the IOUs came from). Every time an IOU is added, everyone’s app will verify the IOU, and when enough of the apps agrees that the IOU is legit, the IOU is stored as a ‘block’ in everyone’s digital notebook.

The other feature is that these blocks are linked, so that no matter how many times the IOU is exchanged (let’s say A owes B, and B owes C – allowing C to claim from A), the origin of the lunch can be traced back. And to encourage participation, the whole class agrees that each time x number of IOU blocks have been verified, those apps that did the verification will get a chance for a treat.

(But seriously, how does it work?)

For a more technical way to explain blockchain, you may want to check out this video (which I previously mentioned).

How does it impact (in a good way)?

Now, the first application of blockchain technology was Bitcoin, founded by Satoshi Nakamoto (an anonymous person whose identity is still a mystery). And since then, a flood of cryptocurrencies were thus born, aimed to substitute traditional means of transacting money (that is through “central nodes” of banks). This would also mean lower transaction costs, and faster transaction speeds.

So far in this post, I have been using the word “transaction”, which may lead to confining the idea to mere financial transactions. In the world of blockchain though, simply replace the word “transaction” to “information”, and the scalability of blockchain’s application would be almost endless.

According to WIRED, biggest advocates believe that blockchains can replace central banks (through cryptocurrencies), and “usher in a new era of online services outside the control of internet giants such as Facebook and Google”. The example they cited was Storj, a startup offering file-storage service by distributing files across a decentralised network.

Also, since no single entity has monopoly over the validity of transactions (as Tony Yin pointed out), there would be no single point of failure, and that no one can cheat the system. Therefore, there is the potential of application in corporate compliance.

Going a step further into the future, WIRED pointed out that our digital identities can be tied to a token on a blockchain, in which we will use this token (that is permanent and verified to be true) to log in to apps, open banking accounts, apply for jobs and even verifying messages. And since the blockchain cannot be tampered with, there are ideas of using blockchains to even handle voting.

Other than that, blockchains can also help in automating tasks. The WIRED article used an example of a will, in which it can be stored in the blockchain (hence replacing notaries), and even be made into a smart contract to automatically execute the will and disburse money to the heirs in the will. A smart contract is a software application that can enforce an agreement without human intervention.

So far, the immense potential of blockchain’s application sounded like the future is here. However, the pace of its arrival may not be as quick as we expect.

What are the issues?

In the readings, I can generally summarise the main issues into three points:

- Adoption requires time

Harvard Business Review in its article compared the adoption of blockchain to the adoption of the TCP/IP protocol. And if that protocol sounds familiar, it is because you ARE on the protocol – the internet. Bear in mind, the technology was introduced in 1972, and its first single-use case was emails among researchers on ARPAnet. We have indeed come a long way in terms of time and concerted effort, going through 4 phases as identified by the article before the protocol transforms to the internet we know today (examples in parenthesis): single use (the emails on ARPAnet), localisation (private e-mail networks within organisations), substitution (Amazon online bookshop replacing traditional brick-and-mortars), and finally transformation (Skype, which changed telecommunications).And this is what Harvard Business Review argues: blockchain, as a foundational technology like the TCP/IP, would also need to go through these 4 phases: single use (Bitcoin payments, which we now see), localisation (private online ledgers to process financial transactions, which is still pretty much in development), substitution (retailer gift cards based on bitcoin), and trnasformation (self-executing smart contracts). Furthermore, the article suggested two dimensions affecting the evolution of the two technologies: novelty (how new it is, which also mean how much effort is required to ensure the users understand what problems the tech solves), and complexity (how much coordination is required to produce value with the technology).In short, it would take a while, even with the rapid pace of technology transformation, because the users would need to take a while to cope with it.

- Decentralised means less-to-no control

When cryptocurrencies gained traction (and the idea of them potnetially replacing fiat currencies gained steam), central banks are generally squeamish (or weary) given the fact that cryptocurrencies, which leverages on the blockchain, have no central banks to speak of, and hence have limited-to-none influence or control on how the cryptocurrencies behave, and its relative impact to the normal fiat currencies. And such fears are also echoed by companies who want to keep a certain amount of control on how information is kept, which leads to the next point of…

- Open means less-to-no privacy

At the moment, there are several financial institutions have begun experimenting the blockchain technology (examples in the next section). But these experiments involve creating “private” blockchains which run on the servers of a single company and other selected partners. This stands in contrast with the blockchains in which Bitcoin and Ethereum operate on – anyone can view all of the transactions recorded on the network. Perhaps this would indeed be the next phase of foundational technology evolution that was spoken of earlier – localisation.But on a more futuristic level, when it comes to a point where we would actually have a digital identity on a blockchain, it would mean all of our data would be in public view to everyone. And let’s say that a nation’s government has created such a blockchain, it would try to remove the pseudonymity out of the picture in the name of national security.On a less futuristic front, there are already privacy issues raised against companies that use blockchain. Bloomberg’s article pointed out that under the European Union’s General Data Protection Regulation, companies would be required to “completely erase the personal data” upon requests of any citizens. Some blockchains’ design may even be incompatible to the said regulation.

On a technical front, some may point out the issue of preventing double spending, or a conflict about a certain transaction in the ledger. To this end, according to Tony Yin, the blockchain technology do not solve the problem, but rather the implementation does via the blockchain’s proof-of-work, or how the solution to the problem is verified. (If you are thinking, what problem needs to be solved, just remember that the blocks are encrypted with mathematical problems).

On a perceptional front, there may be concerns about hacking following several cases of cryptocurrencies and ICOs hacking (e.g. Bitcoin’s Mt. Gox and the DAO hacking mentioned in the previous ICO post). However, if you were to look deeper into these hackings, you will find that while the exchanges in the front-end suffered the attacks, the underlying technology remains intact. Thus, it is important to separate front-end interfaces from underlying technology in discussing about blockchain’s security.

How do we respond?

Indeed, there are organisations that have already begun their journey of using blockchain. According to the WIRED article, the Australian Securities Exchange announced a deal to use the blockchain technology from a Goldman Sachs-supported startup for post-trade processes in the country’s equity market. On the other hand, there are reports of JPMorgan and the Depository Trust & Clearing Corp experimenting with blockchain technology to improve efficiency of trading stocks and assets. These examples show that blockchain technology can be used to solve existing problems with slow transfers beyond payments and remittances.

Harvard Business Review suggested for company executives to “ensure their staffs learn about blockchain”, and to consider developing company-specific applications based on the 4 phases identified, and to invest in blockchain infrastructure.

On a broader level, we as a society would have to address and answer more fundamental questions that the blockchain technology poses when it reaches a greater scale, such as how do we perceive data privacy, and what does it mean to have less central control in a decentralised world.

Meanwhile, the development journey of this technology has only one way to go – up. And we have to embrace the transformation and changes that come along with that development, by getting ourselves more educated about the subject matter, and considering how we can leverage the technology to make lives better.

References

What Is Blockchain? The Complete WIRED Guide – WIRED: https://www.wired.com/story/guide-blockchain/

The Truth About Blockchain – Harvard Business Review: https://hbr.org/2017/01/the-truth-about-blockchain

Is Your Blockchain Business Doomed? – Bloomberg: https://www.bloomberg.com/news/articles/2018-03-22/is-your-blockchain-business-doomed

Explain Like I’m 5: Blockchain (an easy explanation of the technology behind Bitcoin) – Hayley Somerville: https://www.linkedin.com/pulse/blockchain-5th-graders-hayley-somerville/

Blockchain, Bitcoin, and Ethereum ELI5 (Explained Like I’m Five) – Tony Yin: https://tonyy.in/blockchain-eli5/

Featured Image: By B140970324 (Own work) [CC BY-SA 4.0 (https://creativecommons.org/licenses/by-sa/4.0)%5D, via Wikimedia Commons

3 thoughts on “From What I Read: Blockchain”